Free Checking

With Dividends

Put your money to work with a fee-free account that earns.

From pre-approval to closing, our homeownership options make it easy for you to find a place to call home.

Get rates as low as 6.75% APR* on terms that align with your budget.

Get RVs, ATVs, motorcycles, and more with rates as low as 7.25% APR*.

Explore our range of flexible home loan options and take the first step towards homeownership!

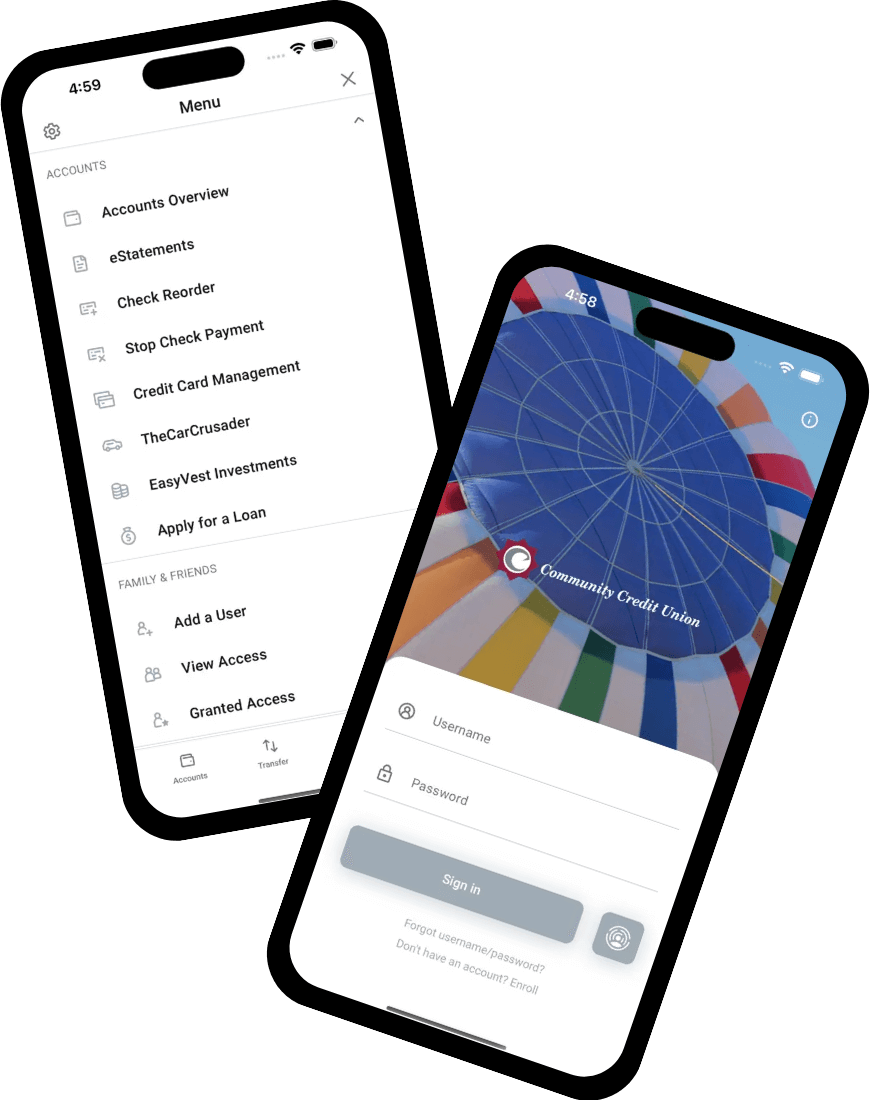

Experience convenient, secure access to your account 24/7 with Digital Banking.